Buying a car is not a huge decision for me. It is for some people, but not for me.

I owned my first car the day I received a license to drive. Actually sooner. As soon as I received a learner’s permit, I was driving around.

Like every hot-blooded teen, I too retained a fascination of cars – particularly fast cars – in my youth. It’s a passion I still harbor to a certain extent. It is indeed fascinating to be able to drive at a heart-thumping velocity. I have owned reliable cars, particularly Hondas, and while those were never racing cars in any sense of the word, I had great fun taking them to risqué speeds way past the limits.

And yet, I won’t be buying one this year… and perhaps even over the next several years.

I used to think of a car as a status symbol. I distinctly remember the feeling of significance as I drove past people in their everyday vehicles whilst handling a sports car myself… one invariably borrowed from a friend and so on. I love it. There’s no denying it. It’s a great feeling.

Of course, there is the A to B function. That is and has been the intrinsic function of having a car. But few if any of us use (or value) a vehicle strictly from the point of being hauled from A to B. It has… and will always be… a status symbol, a chariot on wheels, a home on the road, and a thrill-machine for most.

But I don’t think I’ll be buying one anytime soon.

While I can buy a top-of-the-line vehicle right away… or a super-luxury you’ve-gotta-have-money-burning-holes-in-your-pockets machine like a Rolls Royce in a few years without much financial discomfort, I won’t be buying either. Neither a nice everyday semi-luxurious haul-ass like a BMW nor a super-luxurious Rolls or Lambo Urus.

And no… I won’t be buying a cheapo Camry either.

I just simply won’t be buying a vehicle.

Simply because it makes no financial sense for me.

Now… before I explain that… let’s be clear about one thing. This is how it is for me given my current lifestyle and profession. If things were different, I might as well have picked up some vehicle, as I often have in the past, and might in the unknowable, unforeseeable future.

So here are the top six reasons why I won’t be buying a car in the near future…

1. They say a car is the worst class of asset you can buy. I disagree.

A car isn’t an asset at all. It’s a consumable. It’s a money-pit. The second you drive it off the lot, you lose anywhere between 10% to 30% of its value. In one split second.

Actually, not even after you drive it off the lot. As soon as you sign the paperwork, your $100,000 “asset” is instantly worth $70,000 to $90,000. Before you see it. Before you touch it. It’s worth less money than you just paid for it.

When something loses value that fast… it’s not an asset.

It’s a consumable.

You buy gold, and suddenly it isn’t worth less just on account of you having bought it. You buy real estate and it doesn’t immediately lose a part of its value just because now you own it. Those are assets.

Sure, assets do go up in value… and sometimes even good assets go down in value.

But all that depends upon market forces. Or maybe forces of nature. None of the value is destroyed by you owning an asset.

Now… compare that to a sandwich. You buy a $5 sandwich. You couldn’t turn around and sell it for $4.50 to the net man in the queue. Because he’d rather pay $5 and get his own freshly made one.

So consumables are things that lose value instantly upon ownership. Assets don’t. And as such, a car or a vehicle of any kind must necessarily be classified not as an asset but a consumable.

Now this distinction also applies to your kitchen remodels, by the way. You spend $50,000 on a kitchen remodel, but the appraisal doesn’t go up by $50,000. It goes up by maybe $20,000 if you’re lucky and didn’t get screwed bad.

So a kitchen remodel is a money pit. It’s a consumable.

Next time you hear someone say cars are depreciating assets… tell yourself that they’re not assets at all. Not everything with equity is an asset.

Fundamentally, there are only four kinds of assets in the world:

- Money: Currencies don’t lose value upon change of ownership. Hard or soft. USD or BTC. They may lose value over time based on other factors, but not simply because the ownership changed.

- Stock in corporations: Big, small, whatever. You own a part of the business, and if/when the business produces a profit, you own it. End of story. You can sell your stock, and it won’t lose value just because someone else owns it now.

- Land: The physical structures that we call houses lose value over time. They need to be maintained, and eventually they must be demolished to free up the land so that a new structure may be erected. So houses are depreciating assets. Land on the other hand is largely an appreciating asset. Simply because populations continue to rise, and you can’t just print more land.

- Precious metals and gems: Not diamonds of course. Diamonds are consumables, and grossly over-priced ones at that. The second you decide to buy a diamond you lose wealth. But other gems like rubies and emeralds that are far rarer and much more limited. Or gold. Those things are assets and do not lose value simply by existing. And right now, some of these assets are massively underpriced. In fact, many times it would cost you more to mine an ounce of gold than it sells for if you owned a goldmine.

That’s it. Those are assets. Almost everything else is either a liability or a consumable.

2. A car is both a liability and a consumable.

And while consumables have a place within your budget, they have to make sense.

Which brings me to the second reason why I won’t be buying a car anytime soon…

I don’t eat a lot of bread. Or even any bread at all. Buying a loaf of bread just because it looks nice and is on sale doesn’t really make sense. I won’t be using it for its intrinsic value.

Similarly, I won’t be using the car much if at all.

My goal right now is to get an apartment as close as I can to my place of work so that my commuting time is minimized.

Side note: Did you know that every minute you spend commuting equals one whole day of work over a year.

- 1 minute of commuting time

- Equals two minutes each day back and forth

- Equal 500 minutes per year (assuming 250 business days)

- Equal 8 hours and twenty minutes over the year.

So if your residence is ten minutes away from your place of work, you’re wasting ten business days each year just commuting.

Now I’ve heard there are people who spend two hours each morning from their home to get to work, and then two more hours to get back.

Honestly, that’s 125 full business days worth of commuting every single year. If they then turn around and talk about being trapped in their jobs like hamsters in a wheel or about having their soul sucked out by their mind-numbing jobs… you know why they feel the way they feel.

I am going to rent an apartment right on top of my place of business.

One or two business days wasted annually are bad enough. You can’t put a price on time when your ultimate objective is to free up all your time.

I do live in a big city, and I don’t foresee myself not living in a big city for the next decade, so this wouldn’t really apply if I lived in a small town where it takes several minutes just to get across your own lot.

Therefore, as a professional, I don’t need a car at all. It would only be a waste of time.

I don’t really travel a lot for business, but when I do, it’s generally out of state or out of the country. So a personal vehicle isn’t exactly going to do me a whole lot of good there either.

Then there are the weekends. I don’t always travel outside my city. But when I do, I find it might take less time just picking up a vehicle from Hertz et al instead of getting it out of my own parking garage… especially since they already have my credit card on file and I have a status account with them.

3. A car is a big liability especially in big cities

Financially and emotionally.

==> You gotta rent a garage… which is like renting another place. The rent itself can go all the way up to $1000 a month or more depending upon the vehicle.

==> You still need to find a parking spot if you take your vehicle somewhere in the city. Temporary parking can cost upwards of $20 an hour.

==> On top of that, there are other costs – like insurance, maintenance, fuel (which admittedly is so cheap right now that I feel tempted to buy a car just because of the near-zero fuel prices) and upgrades.

==> There’s always this constant need to care for the vehicle – keeping it clean and so on. People spend hours every week just taking care of their vehicles. Good for them, but just won’t work for me. I value my time too much.

==> You also need to worry about keeping the tank full. Talk about waste of time!

==> You worry about red lights and traffic cops. About renewing your license every few months. About points and lanes. About bad drivers all around you… Let’s face it. Big cities are full of people who don’t know how to drive properly. In many cases people don’t even have proper licenses.

==> You also worry about nicks, dents and scratches. About people who don’t know how to take care of their own vehicles and will ram their doors into the side of your car at a parking lot.

It is enough to make a sane man go crazy.

So you waste time, money AND mental sanity taking care of a vehicle, especially in a big city.

Last year I found an amazing deal on a barely used 2006 Ferrari F430 Berlinetta with less than 25000 miles on the odo… which I was rather sure I could use for a few months and resell it for more than I’d have purchased it for. Then I went to the parking garage near my place to find out how much they’d charge me for parking that vehicle. Since a Ferrari is generally classified as a sports car, the garage alone wanted $1400 a month. When you add in the insurance and maintenance, I’d be shelling out well over $4000 a month even with an awesome deal.

Now… $4000 a month is nothing for a vehicle like that.

But when you take into account I’d get to drive it maybe 4-6 times a month even if I tried to squeeze out every opportunity from my lifestyle (without adversely affecting my work schedule of course) it becomes more sensible to rent it by the hour. Which I have done a couple of times, and I must admit… it’s great fun.

Photo credit: https://findbyplate.com

4. It is a massive waste of time

Getting a car out of a garage and back into a spot can take as much as 10-15 minutes each time, by the way. Which is fine if you’re going to drive for several hours. But not if your driving time is 10-15 minutes before you have to find a spot to park it in again.

Now, if you live in the country, it’s great because you just get in and drive. But for me, an Uber arrives in approximately 2-3 minutes at any time during the day and even at night. I’d be at my destination using Uber by the time I’d get my car out of my garage if I were travelling within the city.

Sometimes, for the sake of saving time, it makes more sense to use Subway than to drive (or be driven around) because of the traffic.

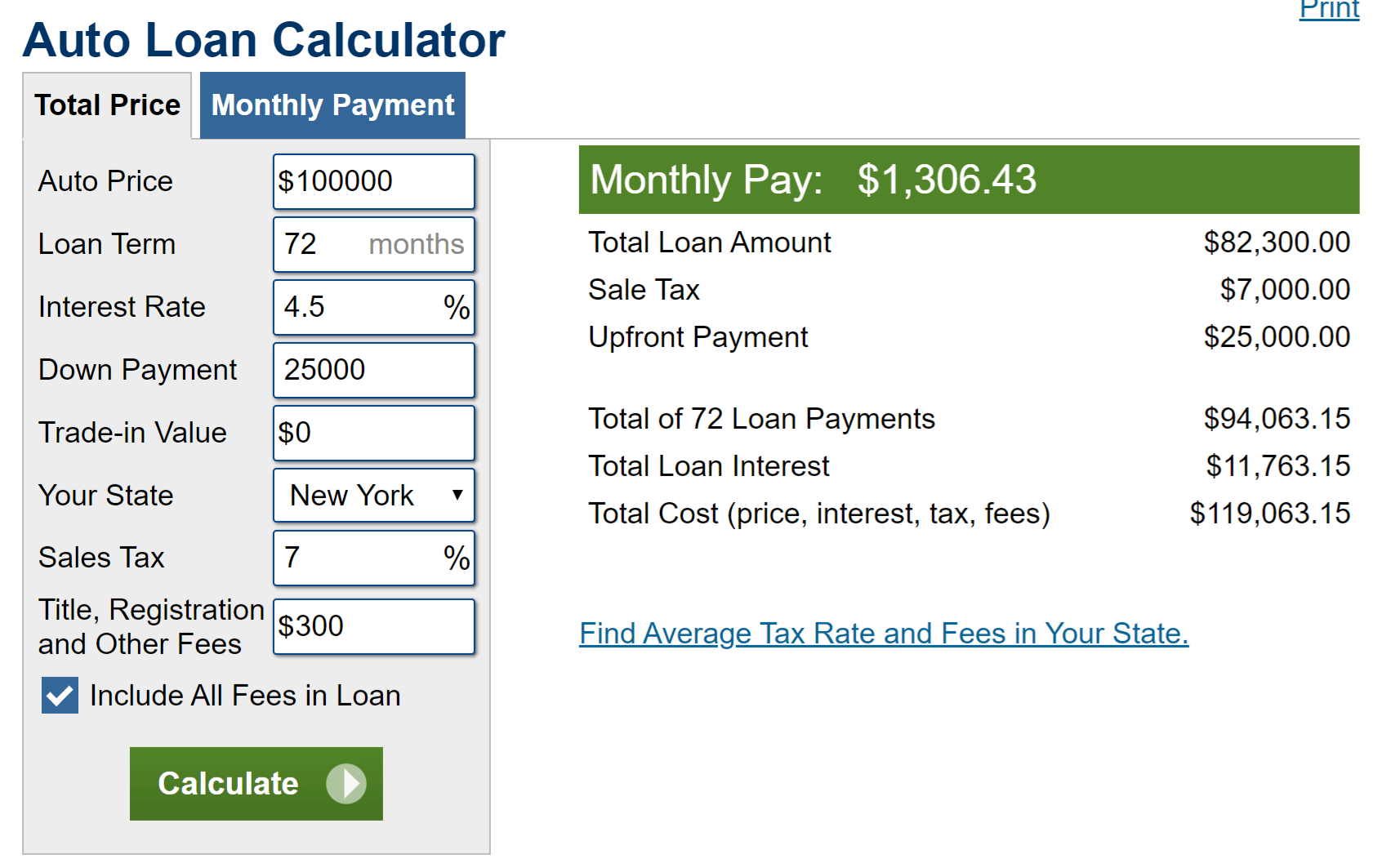

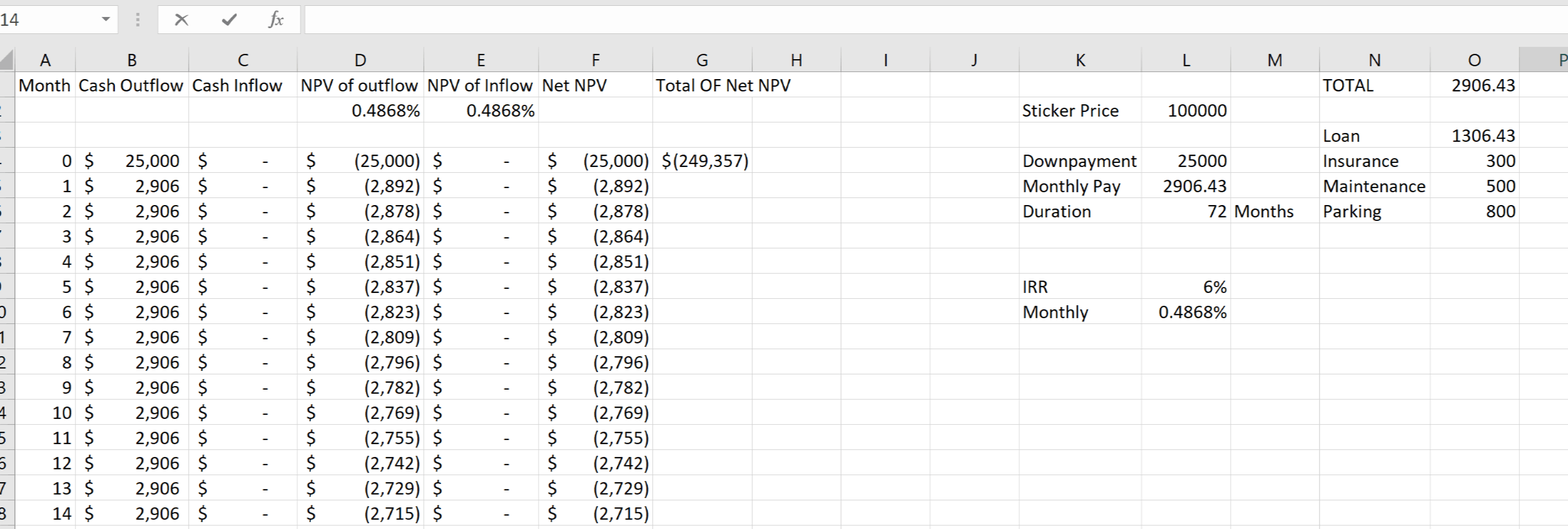

5. It is UNBELIEVABLY Expensive

The net present value of owning a vehicle with $100,000 sticker price is about $250,000 for me. A $100,000 vehicle will cost you $1306.43 a month for 72 months. But that’s just the loan repayment. There are other costs too.

If you take all of those costs into account, and if you assume my money is worth a measly 6% internally (it’s not… because my own internal rate of return is way higher than 6%) then a $100,000 vehicle is actually going to cost me just a hair under $250,000.

You can see the calculations for your self here… https://cloud.westernston.com/geuWprmj

It just doesn’t make fiscal sense.

For $250,000, with leverage I can buy ten single-family homes and rent them out for $1500 to $2000 a month each. After all the expenses (interest, mortgage repayment, taxes, maintenance, management, vacancies) I’d still end up with $12,000 to $20,000 a year in net profit. This number grows over time because of rental increases.

Which is more than enough to pay for all the Uber rides I could use over the year. I could take as many as 300 rides in Uber each year at $50 a ride (so we’re talking luxury sedans or SUV’s here) but I really don’t need that many.

Not to mention the growth of equity as a result of mortgage repayment. Then there is the appreciation on account of demographics as well as inflation. I’d be getting a net profit of well over $50,000 to $80,000 a year even after paying for all the Uber rides.

My initial investment would at least double… maybe even triple over ten years, producing an internal rate of return of well over 20%. With as many Uber rides as I need in luxury vehicles. And hours upon hours saved every month. And zero stress or anxiety. Zero obligations.

Should I fall upon hard times cashflow-wise… I don’t need to necessarily user luxury Ubers when a simply Subway ride would suffice. You can get unlimited subway rides for $130 a month in New York.

And by the way, I just realized I didn’t even account for other parking charges. You don’t just pay for a spot in your own garage, you also pay for parking at wherever you take your vehicle. But I’m too lazy to go back and add those numbers in, so I won’t. Of course, those numbers would add several thousands even tens of thousands) of dollars to the net present value of the cost of ownership of the vehicle.

6. It’s a distraction

I have professional goals.

They aren’t massive or anything, but they do include getting to a point of total financial freedom within a number of years that you can count on your fingertips.

In other words, I’m working towards having passive income that outdoes my monthly expenditure by 3-5x (and growing) over the next few years. My expenses aren’t small, nor do I intend to lead a particularly frugal life.

If I were to plonk down $250,000 (or even just $50,000) on a vehicle today, I’d feel guilty if I didn’t use it frequently enough. I’d end up driving and taking trips just for the heck of it. Why? Because I just spent the money… that’s why.

And ultimately, it would distract me from focusing my entire energy on my singular goal.

Consequently, the ownership of this vehicle would set me back by at least 5-10 years in the overarching objectives that I currently am pursuing.

Ain’t no way on this God’s green earth I am going to let that happen.

So…

In conclusion, I will not be buying a car until I get to the end of my professional marathon. I fully intend to retire within the next 10 years or even sooner… and a car can do nothing but derail me from that objective at this point.

Now, I do fully intend to purchase a car.

Not right now, of course. But once I do retire, I will be purchasing a car. Here’s why:

- I’ll be working with a significantly bigger budget. As far as lifestyle upgrades go, a nice car is just something I am going to spend a great deal of money on. But money that I can afford to spend free of guilt.

- I’ll be buying a VERY nice car. I can’t really predict which one. But it’d necessarily have to be the kind of car kids salivate over. Simply because I’ll just “need” luxury for my intended use-case.

- I’ll actually have a use for it. I do intend to get out of the city and travel the world. I will be using a car for the most part, because I’ll spend several years just driving from one place to the next with no itinerary. Living there as long as I need to before I get bored and move on. I’ll need a lot of space in the car, and I’ll need a lot of creature comforts. I’ll be actually putting the wheels to good use.

- Everything’s easier and faster when you’re on the road. Refueling takes a couple minutes. Wash takes maybe ten. There are repair shops all over should I need one. Parking is abundantly available outside big cities. Mostly it’s free. Time wise, it becomes so much more economical than waiting in lounges and queues taking a flight. Plus, it’s cheaper and it’s fun. And ultra luxurious too, at least for the kind of car I’d be buying.

It would make perfect sense for me at that time.

But for now, a car is something I just won’t be buying. It can only cost me dearly. And it can only slow me down.

I would buy it if I didn’t live in a big city, but I do. And as such, I can rely very well on Ubers and public transport. Plus the occasional rental.

So that’s what I’m doing.

F430 – nice choice. Ppl are WAY too mileage-sensitive on those however. I really need to sell some cars and be more liquid but man is it hard after you restore them yourself 😛

They are also currently outperforming my crypto portfolio by a healthy margin.. hmm may need to get more cars

You can get a better job if you have a car. You also don’t lose it as easily as someone who doesn’t have his or her own car.